Carbon Taxes

The curious case of Belgium’s counterproductive household energy taxes

Beginning of November, many Belgian political parties reacted strongly to the policy letter of the new Federal Minister of Climate who advocated the immediate introduction of a Carbon Tax. Reactions ranged from ‘not Belgium but Europe should introduce carbon tax’ over ‘anti-social’ to ‘just another tax increase’.

Household energy taxes

What the many reactions had in common, however, was the misunderstanding that already today, in Belgium, almost every energy carrier is (sometimes heavily) charged with a wide set of levies, taxes, and duties that could be considered as indirect carbon taxes — albeit very counter-productive carbon taxes:

- Household electricity bills include 0.072 €/kWh of regional earmarked taxes linked to subsidies for renewables and social obligations of the grid operators and suppliers, include 0.051 €/kWh of federal levies, and charge VAT on top of both. These charges account for 37% of the total unit price of 0.27 €/kWh. With an average specific emission of 250 gCO₂/kWh and a European carbon tax of 30 €/tCO₂ yet included in the commodity component through EU ETS, this translates into an implicit carbon tax of 400 €/tCO₂.

- Household gas bills include 0.0012 €/kWh of regional earmarked taxes linked to social obligations of the grid operators and suppliers, 0.0016 €/kWh of federal levies, and charge VAT on top of both. These charges account for 11% of the total unit price of 0.052 €/kWh. With specific emissions of 195 gCO₂/kWh, this results in an implicit carbon tax of 29 €/tCO₂.

- Household fuel oil prices include 0.009 €/l in federal earmarked taxes, and 0.019 €/l in duties. These charges account for 7% of the total unit price of 0.47 €/l. With specific emissions of 2640 gCO₂/l, this results in an implicit carbon tax of 13 €/tCO₂ — or 10 €/tCO₂ if you account for the emissions generated during the production, refining, transport, and storage of the fuel oil.

- Petrol prices include a 0.60 €/l of excise duties and charge VAT on top of these duties. These charges account for 52% of the total unit price of 1.41 €/l. With specific emissions of 2390 gCO₂/l, this results in an implicit carbon tax of 307 €/tCO₂ — or 237 €/tCO₂ if you account for the emissions generated during the production, refining, transport, and storage of the petrol.

- Diesel prices include 0.60 €/l of excise duties and charge VAT on top of these duties. These charges account for 53% of the total unit price of 1.38 €/l. With specific emissions of 2640 gCO₂/l, this results in an implicit carbon tax of 278 €/tCO₂ — or 210 €/tCO₂ if you account for the emissions generated during the production, refining, transport, and storage of the diesel fuel.

- LPG is not subjected to excise duty while having an average unit price of 0,48 €/l. Hence, despite specific emissions of 1665 gCO₂/l, they are charged an implicit carbon tax of 0 €/tCO₂.

Summarizing the above gives the following graph:

These obligations, levies, and excise duties in the energy prices already take a significant party of a household budget:

In Belgium, annually, an average household consumes 3.5 MWh of electricity, burns 23 MWh of natural gas for heating and domestic hot water, and drives approximately 15 000 kilometers in a diesel car. For this energy use, it pays a total of 3185 €, of which 1000 € (or 32%) are taxes and duties:

- 320 € for its electricity use, 130 € for heating, and 550 € for driving.

- 285 € of regional public service obligations, 55 € of charges, 450 € of federal excise duties, and 210 € of VAT charged on top of the charges and duties.

For a total of 7.5-8.1 tCO₂ of greenhouse gas emissions, this averages an implicit carbon tax of 120–130 €/tCO₂ — a number very similar to the carbon tax of 110 €/tCO₂ in Sweden, for example.

But the current taxation of energy carriers also has some perverse effects:

- First, no one really knows whether the current distribution of taxes between different energy sources is socially correct or protects households against energy poverty.

- Second, the high charges on electricity are radically thwarting the intended energy transition: For mobility, we generally aim to switch from internal combustion engine (ICE) vehicles to electric vehicles (EVs), while Belgium taxes the energy consumption of ICEs noticeably more favorably compared to charging EVs. The same counts for heating where we generally aim at a transition from fossil fuels such as natural gas and gas oil to electric heat pumps, while Belgium charges the consumption of these fossil fuels radically more favorably than the heat pump.

On top of that, Belgium mainly focuses on soft measures to realize both transitions.

Taxing the energy transition

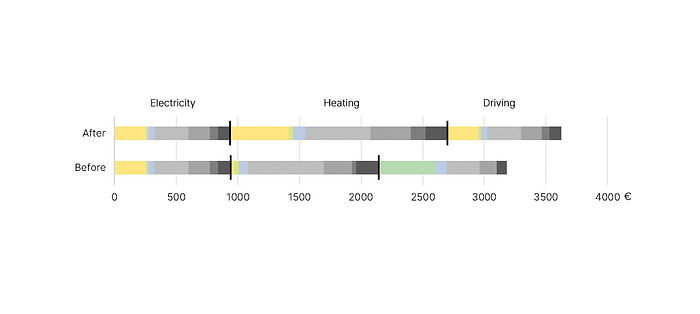

The impact of the skewed taxation on the intended transitions becomes clear when we calculate the energy bill of a household that invested in a heat pump and an electric car. If the same Belgian household as described above generates its heat demand with a heat pump with an SPF of 3.5 and travels the same amount of kilometers with an electric car, it would have an annual energy bill of 3675 € (+15%), of which 1250 € (+25%) are local taxes and duties:

- 320 € for its daily domestic electricity use, 610 € (+360%) for heating, and 320 € (-40%) for driving.

- 980 € (+244%) of regional public service obligations, 70 € (+27%) of charges, no federal excise duties, and 200 €(-5%) of VAT charged on top of the charges and duties.

For a total of 3.4 tCO₂ (-60%) of greenhouse gas emissions, this averages an implicit carbon tax of 370 €/tCO₂ excluding EU ETS.

For a household, the switch to the best available technologies would result in an absolute increase of the total energy bill of +450 €, including an absolute increase in taxes and duties of +250 € per year — for a decrease in annual emissions of 4.9 tCO₂/yr. In this situation, the only way the same household could end up having the same annual household energy bill is by reducing its energy demand for heating by 30% through insulation — further reducing its footprint to 2.9 tCO₂.

The Flemish Government grants up to 1500 € in subsidies for the installation of a residential air-water heat pump, but then taxes the electricity to run the same heat pump with up tot 600 € per year. In this context, the Flemish government has budgeted over 30 M€/yr of subsidies for green heat, while it taxes the same green heat with 1400 M€/yr through regional (earmarked) taxes in the electricity bill.

Takeaways

Belgium’s search for a significant, impactful carbon tax does not, therefore, require any tax increase: with over 2 billion euros in regional taxes on the electricity and natural gas bills and over 6 billion euros in excise duties on fuels, energy is already heavily taxed — yet not in a smart way. A well-considered, gradual reform and shift of all energy taxes could in itself start a major carbon revolution …